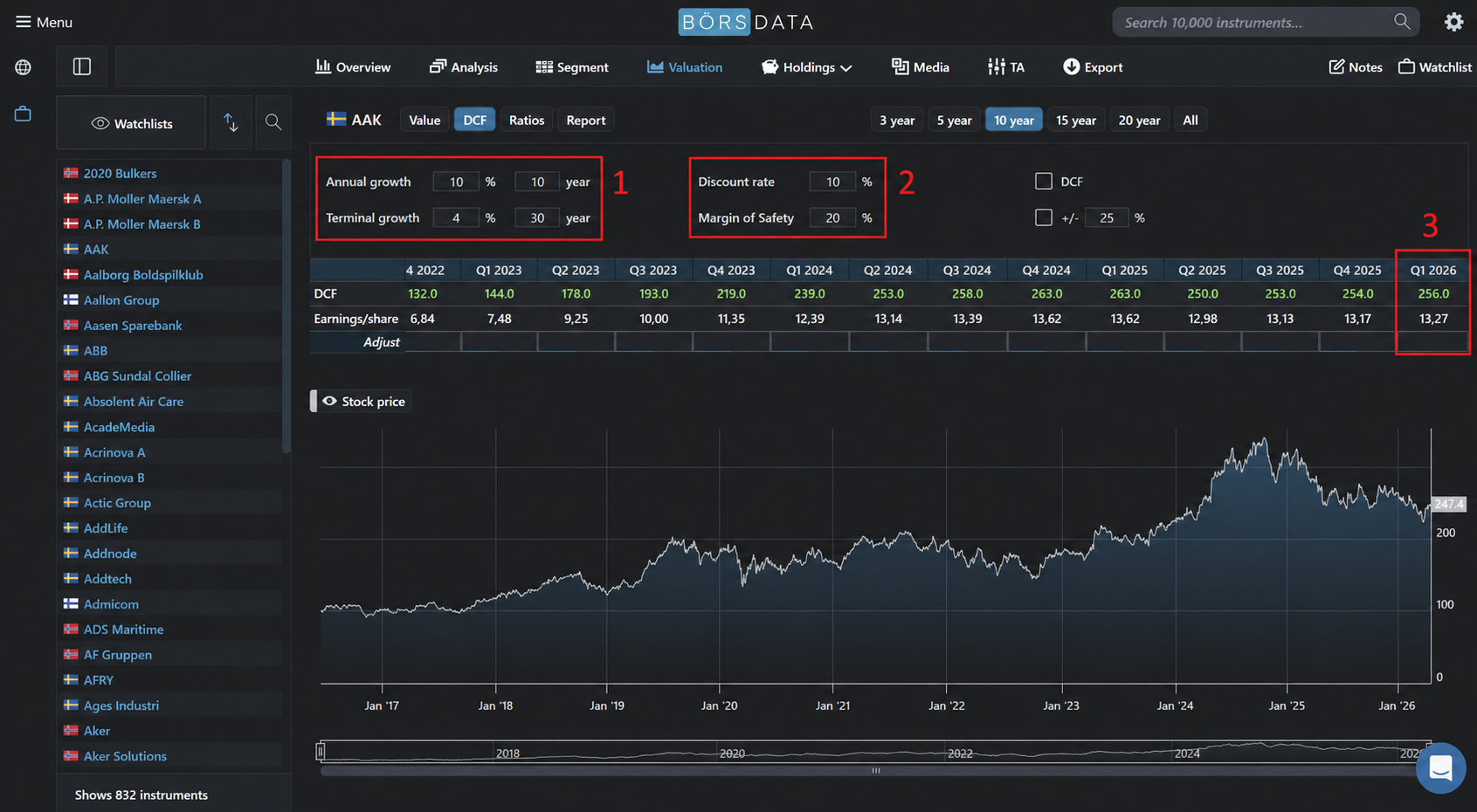

DCF - Discounted cash flow

What is DCF?

Simplified, Discounting means that we calculate what SEK 100 in 10 years is worth today. That is, we count backwards and include a certain return each year. This means that the higher the return we expect, the lower today's value will be.

A share that we believe will grow by 20% each year will have a higher value today, than a company that will only grow by 5%.

Overview

DCF can calculate a reasonable value of what the company should be valued at, depending on the company's current profit, growth rate and required return.

The unique thing is being able to see the company's current and historical valuation together with the share price development over time. This makes it possible to compare the company's reasonable valuation in relation to the market value. It makes it easier to see over- and under-valuations.

DCF - Discounted cash flow

DCF is the most widely used valuation model in the financial industry. It is about discounting future cash flows to a value today. Three important parts that you have to adjust after each company.

- growth for all companies is 10% by default for all listed Companies.

It is important that annual growth is adjusted to a more reasonable growth rate for the current company. Annual growth is calculated up to 10 years and after that it is the terminal growth takes over. Carefully using high growth values.

-

the discount rate is the same as the return requirement of the Investment. Lower yield requirements generate higher valuations and equally so a higher yield requirement results in a lower Valuation. Do not change if you are not sure what is a reasonable return requirement.

-

the latest rolling profit must also be adjusted if it does not reflect a fair profit level on the Company. There are many reasons why the reported profit shows unreasonable levels such as accounting effects on write-downs or revaluations or temporary non-recurring items that affect profits significantly.